Two Owners, Same $200,000 Shareholder Loan

A shareholder loan from your CCPC is either a few-thousand-dollar planning tool or a six-figure CRA reassessment — depending on four decisions made in the first week. Here are two Calgary owners who took the same loan and landed on opposite ends.

Priya took a $200,000 shareholder loan from her Calgary CCPC in January to fund a personal real estate down payment. She had a promissory note, a repayment plan, and a planner who flagged the calendar deadline twelve months in advance. Total cost: roughly $2,800 of imputed-interest tax for the year. The loan was repaid on schedule, the documentation was clean, and CRA never asked a question.

Marcus took the same $200,000 from his corporation the same month for the same reason. No promissory note, no repayment plan, and the first person who mentioned the deadline was his accountant — fourteen months later, when the deadline had already passed. Total cost: roughly $96,000 of personal tax, plus arrears interest running from the original balance-due date, plus an audit that uncovered three years of undocumented personal expenses on the corporate credit card.

Same loan. Same amount. Same city. The difference was four planning decisions Priya made in the first week and Marcus never made at all. Those four decisions are what this post is about — not the compliance mechanics (your CPA owns those), but the planning choices that determine whether a shareholder loan is a smart use of corporate capital or a six-figure mistake.

Key Takeaways

- A shareholder loan is a planning tool, not a workaround. Used correctly — with documentation, a repayment calendar, and prescribed-rate interest — it gives you temporary access to corporate capital at a cost of a few thousand dollars a year. Used incorrectly, it generates $96,000+ of personal tax on a $200,000 loan.

- The repayment deadline is tied to the corporation’s fiscal year-end, not the loan date. Miss it by a single day and the full principal is added to your personal income in the year the loan was made — retroactively.

- Documentation is a planning decision, not a year-end chore. A two-page promissory note signed on the day the loan is advanced costs you 30 minutes. Producing it after a CRA audit notice arrives costs you credibility and usually the assessment.

- The “repay and redraw” cycle is the fastest way to trigger an audit. CRA’s 2025 interpretive folios tightened expectations on the “series of loans” test. Cyclical loan accounts are increasingly being lost at the Tax Court.

- Your CPA files the T-slips and computes the benefit. Your planner designs when, how much, and on what terms you access corporate capital — and whether a loan is the right mechanism at all.

What I do, what your CPA does

This post is the planning conversation. My role is the upstream design — whether a shareholder loan is the right way to access corporate capital for a specific purpose, how much to borrow, on what terms, and how the loan fits into your broader compensation and liquidity plan. Your CPA owns the downstream execution: computing the imputed-interest benefit under section 80.4, issuing the T4 or T5, tracking the repayment deadline, and documenting the loan account in the corporate financials. I don’t file the T-slips. I make sure the structure is one your CPA can file cleanly.

On this page

- Two Owners, Same $200,000 Shareholder Loan

- Key Takeaways

- The Shareholder Loan Worked Example

- Decision 1: Is a Shareholder Loan the Right Mechanism?

- Decision 2: What Goes on Paper Before the Money Moves?

- Decision 3: When Does the Repayment Clock Expire?

- Decision 4: How Do You Extinguish the Loan Before the Deadline?

- The 4 Decisions at a Glance

- The Three Planning Failures I See Most

- Sources

- Frequently Asked Questions

- Conclusion and Next Steps

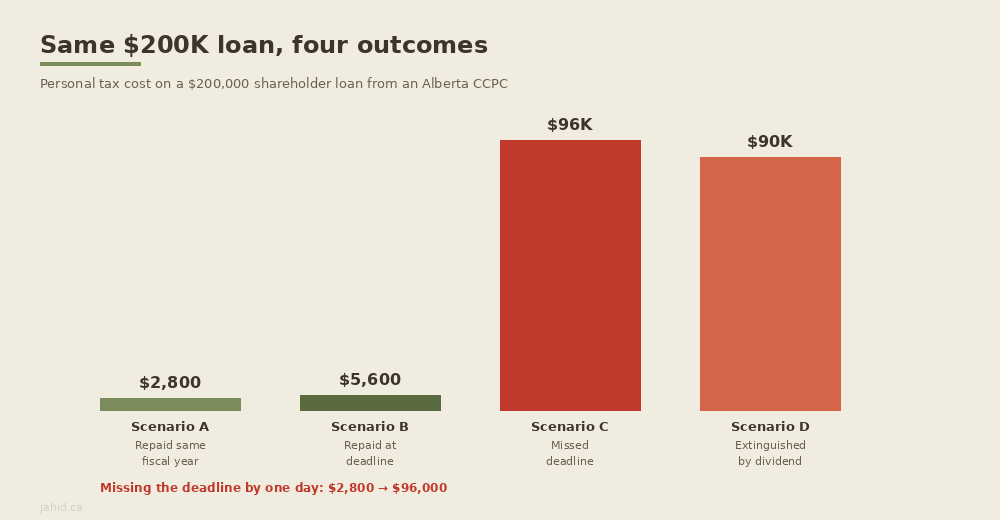

The Shareholder Loan Worked Example: $200,000, Four Scenarios

Before the decisions, the numbers. Same $200,000 loan from an Alberta CCPC with a December 31 fiscal year-end, advanced January 15, 2026. The shareholder is in the top combined Alberta marginal bracket (48% on ordinary income; ~42.31% on non-eligible dividends). The Q2 2026 prescribed rate is 3%.

| Scenario | Repayment timing | Full income inclusion? | Total personal tax cost |

|---|---|---|---|

| A — Repaid Dec 31, 2026 | Within the corporation’s fiscal year | No | ~$2,800 (imputed-interest benefit only) |

| B — Repaid Dec 31, 2027 | One day before deadline | No | ~$5,600 (two years of imputed interest) |

| C — Repaid Dec 31, 2028 | Missed deadline by one year | Yes — full $200,000 added to 2026 income | ~$96,000 + arrears interest + potential audit |

| D — Extinguished by dividend, Dec 2027 | Constructive repayment via non-eligible dividend | No — but dividend is fully taxed | ~$90,000 (dividend tax, no better than never borrowing) |

The verdict. Scenarios A and B cost a few thousand dollars of imputed-interest tax — the cost of temporarily using corporate capital. Scenario C is catastrophic: missing the deadline by a single day triggers a $96,000 retroactive income inclusion. Scenario D is the realistic exit strategy when you cannot repay in cash, but it converts a tax-deferred use of capital into a fully-taxed dividend — usually inferior to having drawn the same amount as dividend in the first place. The difference between A and C is not tax knowledge. It is four planning decisions made (or not made) in the first week.

Decision 1: Is a Shareholder Loan the Right Mechanism?

Before documenting the loan, before computing the interest, the first planning question: should you be borrowing from your corporation at all, or is there a better way to get the money?

A shareholder loan makes sense when three conditions are met. First, you need a specific, episodic amount of capital — a real estate down payment, an investment in another business, a one-time personal expenditure — not ongoing living expenses. Second, you have a credible plan to repay within the one-year window, either from personal cash flow or by declaring an offsetting salary or dividend. Third, the imputed-interest cost (3% prescribed rate in Q2 2026) is cheaper than the alternative — which usually means cheaper than drawing down a personal line of credit or triggering a large personal tax bill by pulling salary or dividends all at once.

When a shareholder loan does not make sense: when you are using it to fund ongoing personal expenses month after month, when the loan balance grows year over year with no documented repayment, or when the “loan” is really a disguised distribution that you have no intention of repaying. In those cases, a salary or dividend — drawn deliberately, taxed once, and done — is cleaner, cheaper after audit risk is priced in, and keeps the corporate books honest.

Shareholder loan

A loan or other indebtedness from a corporation to its shareholder (or a person connected to the shareholder), governed by the shareholder-loan provisions of the Income Tax Act. If not repaid within one year after the end of the corporation’s fiscal year in which the loan was made, the full principal is included in the shareholder’s personal income for the year the loan was taken.

The planning lever: The decision to borrow from your corporation — versus drawing salary, declaring a dividend, or using personal credit — is a compensation-planning decision that sits alongside your salary-vs-dividends strategy. I model the after-tax cost of each option for your specific situation. Your CPA executes whichever path we choose.

Decision 2: What Goes on Paper Before the Money Moves?

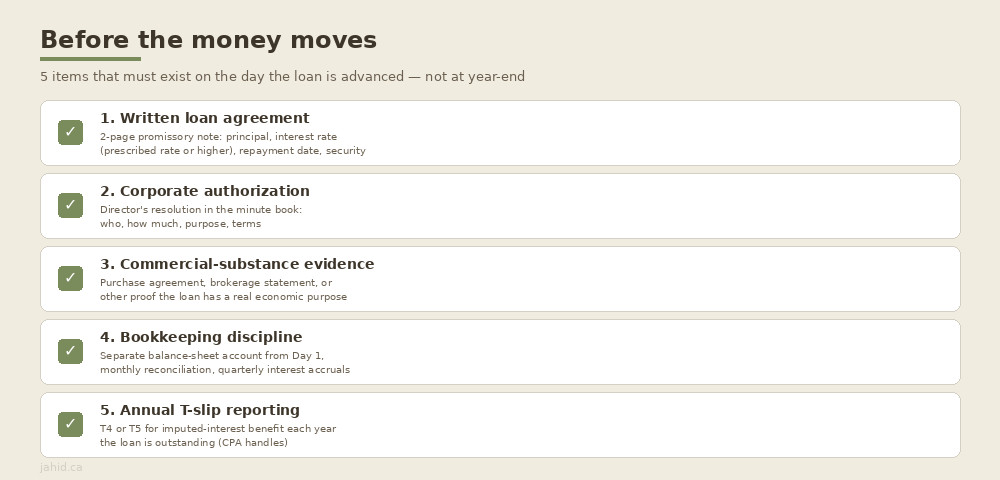

Documentation is not a year-end chore. It is a planning decision made on the day the loan is advanced — and it is the single most common point of failure on CRA audit.

A compliant shareholder loan needs five things in the file, all created before or on the day the money moves:

1. A written loan agreement. A simple two-page promissory note signed by both the corporation (typically by the sole director) and the shareholder. States the principal, the interest rate (the prescribed rate or higher), the repayment date, and any security. Elaborate facility agreements are rarely necessary for an owner-manager corporation. Two pages, thirty minutes, done.

2. Corporate authorization. A director’s resolution or board minute approving the loan — who is borrowing, how much, for what purpose, on what terms. Filed in the corporate minute book contemporaneously. CRA requests the minute book on audit; an empty minute book is a finding in itself.

3. Commercial-substance evidence. If the loan funds a specific use — a real estate purchase, an investment — the supporting documents (purchase agreement, brokerage statement) should be retained alongside the loan agreement. The point is to demonstrate the loan was a real transaction with a real economic purpose, not a disguised distribution.

4. Bookkeeping discipline. The loan appears as a separate balance-sheet account from inception, with monthly reconciliation against the agreement. Interest accruals recorded quarterly. Repayments deposited to the corporate bank account, not netted against other entries.

5. Annual T-slip reporting. If you are not paying prescribed-rate interest (which would eliminate the imputed benefit), the corporation must issue a T4 or T5 reporting the imputed-interest benefit each year the loan is outstanding. Your CPA handles this — but only if they know the loan exists, which brings us back to Decision 1.

The planning lever: I flag the documentation checklist at the same time we decide the loan makes sense — before the money moves, not at year-end. Your CPA prepares the T-slips and reconciles the loan account. The lawyer is only needed if the loan is unusually large or secured by real property.

Decision 3: When Does the Repayment Clock Expire?

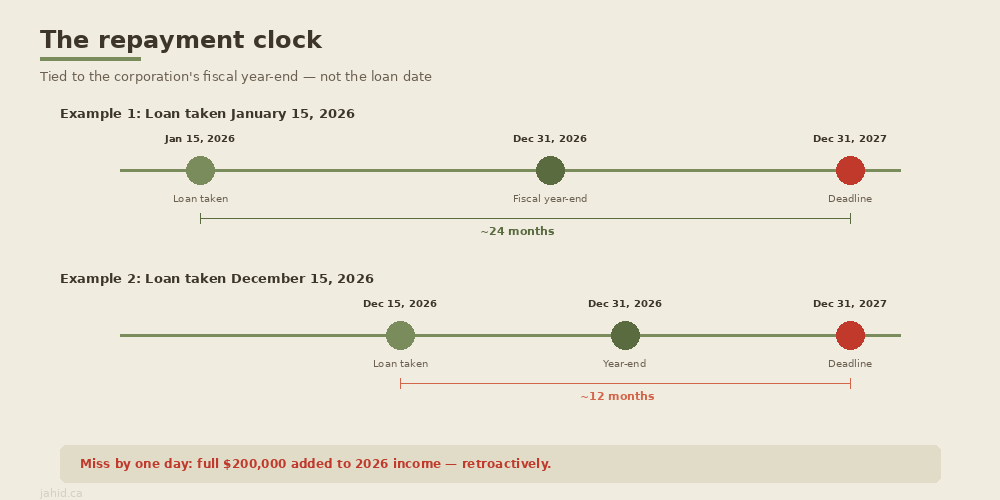

The repayment deadline is the most misunderstood calendar date in Canadian small-business tax. It trips up more owners than any other shareholder-loan provision, and the arithmetic is worth slowing down for.

The deadline is keyed to the corporation’s fiscal year-end, not the loan date. You have until one year after the end of the fiscal year in which the loan was made to repay it.

Worked example: Your corporation has a December 31 fiscal year-end. You take a $200,000 loan on January 15, 2026. The loan was made in fiscal 2026, which ends December 31, 2026. The repayment deadline is one year after that — December 31, 2027. You effectively have just under 24 months from the date the loan was made.

Now flip it: you take the same loan on December 15, 2026 — two weeks before year-end. The deadline is still December 31, 2027 — but now you have only just over twelve months. Same deadline, different runway, because the clock is tied to the fiscal year, not the loan date.

If you miss the deadline: The full $200,000 is added to your personal income for 2026 — the year the loan was made, not the year you missed the deadline. You must amend your 2026 return, with arrears interest running from the original 2026 balance-due date. When you eventually repay in a later year, a deduction is available — but only if you have sufficient other income that year to absorb it. For a founder who has retired or whose income has dropped, that deduction may be only partially useful, making the income inclusion a permanent cost.

The one-year repayment rule

A shareholder loan must be repaid within one year after the end of the corporation’s fiscal year in which the loan was made, and the repayment must not be part of a series of loans and repayments. Miss the deadline and the full principal is included in your personal income for the year the loan was taken — retroactively.

The planning lever: I put the repayment date in the planning calendar on the day we decide to take the loan — not at year-end. A calendar reminder 90 days before deadline gives you time to arrange the repayment source (personal cash, salary, dividend). Your CPA confirms the deadline against the corporation’s fiscal year-end and tracks it in the corporate file.

Decision 4: How Do You Extinguish the Loan Before the Deadline?

You have the loan, the documentation, and the calendar date. The fourth planning decision: how will you actually repay it?

Option A — Cash repayment. Deposit personal funds to the corporate bank account. Cleanest option. The loan disappears from the balance sheet, and the only tax cost is the imputed-interest benefit for the period it was outstanding. This is the plan for owners who took the loan for a specific, temporary purpose and have the personal liquidity to repay.

Option B — Salary offset. Declare a year-end bonus or salary payment large enough to offset the loan balance. The bonus is processed through payroll with withholdings, T4 reporting, and CPP contributions. The net salary flows to you; you immediately repay the loan. Economically, you have converted the loan into salary — taxed at your marginal rate, but generating RRSP room and CPP entitlement. Your CPA must ensure the bonus is actually paid within 180 days of the corporate year-end for the corporation to claim the deduction.

Option C — Dividend offset. Declare a non-eligible dividend equal to the loan balance. The dividend is taxed at your personal rate (~42.31% in Alberta on non-eligible dividends). This is usually the worst option — it converts what was a tax-deferred use of corporate capital into a fully-taxed distribution, with no RRSP room or CPP benefit. It is typically inferior to having drawn the same amount as dividend in the first place. Use this only when cash repayment and salary are not available.

Option D — Prescribed-rate interest (eliminate the imputed benefit, keep the loan). If you want to keep the loan outstanding longer, pay interest at the prescribed rate (3% in Q2 2026) to the corporation within 30 days of year-end. The imputed-interest benefit drops to zero. The corporation includes the interest in its income, but the personal-level cost disappears. For high-balance, longer-duration loans, this saves several thousand dollars per year of personal tax. The documentation is straightforward: a loan agreement at the prescribed rate and a calendar of quarterly interest payments.

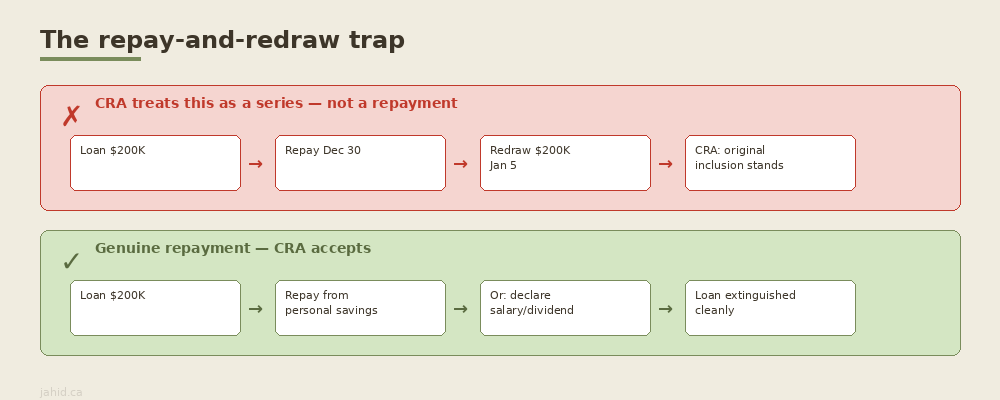

The trap to avoid — the “repay and redraw” cycle. Repaying the loan on December 30 and re-borrowing the same amount on January 5 is not a repayment. CRA’s 2025 interpretive folios expressly tightened expectations on this pattern. If the repayment is funded by another draw from the same corporation, or followed shortly by a redraw of substantially the same amount, CRA treats it as a “series of loans” — and the original income inclusion stands. The test is economic substance: was the repayment real, and was the subsequent loan a genuinely new transaction?

The planning lever: The repayment strategy is part of the original loan design, not a December scramble. When I model the loan, I model the exit at the same time — which of Options A through D will be available to you at the deadline, and which produces the best after-tax outcome given your compensation strategy for the year.

The 4 Decisions at a Glance

| Decision | The planning test | Who owns it | Cost of getting it wrong |

|---|---|---|---|

| 1. Is a loan the right mechanism? | Do you need episodic capital with a credible repayment plan — or is this really ongoing compensation? | Planner models alternatives | Ongoing loan balance → growing audit risk + imputed-interest cost every year |

| 2. What goes on paper? | Is the promissory note, board minute, and commercial-substance evidence in the file before the money moves? | Planner flags; CPA/bookkeeper documents | No documentation → CRA recharacterizes as appropriation → double tax, no deduction |

| 3. When does the clock expire? | Is the repayment date in the calendar, with a 90-day warning? | Planner calendars; CPA confirms fiscal-year-end math | Miss deadline by one day → full principal included in income retroactively |

| 4. How do you extinguish it? | Cash, salary offset, dividend, or prescribed-rate interest — which option fits the compensation plan? | Planner designs; CPA executes payroll or dividend | December scramble → “repay and redraw” trap → audit |

The Three Planning Failures I See Most

After working with CCPC owners in Calgary, three shareholder-loan patterns account for the majority of avoidable damage. Each one is a planning gap, not a compliance error — the CPA cannot fix what the planner never designed.

Failure 1: The loan that was never meant to be a loan. The owner uses the corporate credit card for personal expenses — groceries, vacations, a home renovation — and the bookkeeper quietly parks the charges in the shareholder loan account at year-end. There is no promissory note, no board resolution, no repayment plan. It is not a loan; it is a stream of undocumented personal distributions. CRA treats it as a shareholder appropriation — taxed at full personal rate with no corporate deduction. The fix is upstream: a compensation plan that gives you enough personal cash flow (salary, dividends, or both) so you never need to use the corporate card for personal spending.

Failure 2: The loan balance that grew quietly for three years. The shareholder loan account on the corporate balance sheet increased every year — $80,000, then $130,000, then $200,000 — with no documented repayment and no T-slip reporting the imputed-interest benefit. CRA’s risk-scoring engine flags growing loan balances with no offsetting benefit reported. The audit opens the current year and then reaches back the standard three-year reassessment window. By the time the accountant is involved, the exposure is six figures. The fix: monthly bookkeeping that reconciles the shareholder loan account in real time, not at year-end.

Failure 3: The December 30 repayment that wasn’t. The owner repays the full loan balance on December 30 — funded by a new draw from the same corporate account on January 5. The on-paper repayment is not an economic repayment; CRA treats the cycle as a “series of loans and repayments” and the original income inclusion stands. The 2025 CRA folios tightened this position, and the cases that go to the Tax Court are increasingly being lost by the taxpayer. The fix: genuine repayment from an independent source (personal savings, a declared salary, a bona fide dividend), with no redraw of the same amount in the following weeks.

Sources

The statutory provisions referenced in this post (for readers and professionals who want the primary text):

- Income Tax Act — Section 15 (Shareholder benefits and loans)

- Income Tax Act — Section 80.4 (Loans — deemed interest benefit)

- Income Tax Act — Paragraph 20(1)(j) (Recovery deduction on repayment)

- CRA — Income Tax Folio S3-F1-C1, Shareholder Loans and Debts (effective April 10, 2025)

- CRA — Income Tax Folio S3-F1-C2, Deemed Interest Benefit on Shareholder Loans and Debts (effective April 10, 2025)

- CRA — Prescribed interest rates (quarterly table)

Frequently Asked Questions

What happens if I don’t repay my shareholder loan within the deadline?

If you do not repay your shareholder loan within one year after the end of the corporation’s fiscal year in which the loan was made, the full principal is included in your personal income — added to the year the loan was made, not the year you missed the deadline. For an Alberta resident at the top combined marginal rate of 48% in 2026, a $200,000 unrepaid loan generates roughly $96,000 of personal tax, plus CRA arrears interest running from the original balance-due date. When you eventually repay, a deduction is available in that later year — but only if you have enough other taxable income to absorb it. The planning fix: put the repayment date in the calendar on Day 1, with a 90-day advance warning, and design the repayment source (cash, salary, or dividend) as part of the original loan plan.

How does the CRA calculate the prescribed interest benefit on a shareholder loan in 2026?

CRA calculates the imputed-interest benefit by applying the quarterly prescribed rate (3% in Q2 2026) to the average outstanding loan balance, then subtracting any interest you actually paid in the year or within 30 days of the corporation’s fiscal year-end. For a $200,000 loan outstanding for a full year at 3%, the gross benefit is $6,000; at the top Alberta combined rate of 48%, the personal tax cost is approximately $2,880. You can eliminate the benefit entirely by paying interest at the prescribed rate to the corporation — the corporation includes the interest in its income, but your personal-level imputed benefit drops to zero. Your CPA computes the benefit and issues the T-slip; the planning decision is whether to pay prescribed-rate interest to eliminate the cost.

Can I take a shareholder loan from my corporation to buy a house?

Yes — but it is governed by the same one-year repayment rule and imputed-interest benefit as any other shareholder loan. A narrow exception exists for employee-shareholders who own less than 10% of any class of shares, but this does not apply to a typical CCPC owner-manager. The practical reality: the loan must still be repaid within the deadline to avoid full income inclusion. The planning question is whether a shareholder loan is cheaper than the alternatives (personal line of credit, mortgage, drawing salary or dividends to fund the down payment). In many cases, drawing a salary large enough to fund the purchase — taxed once, generating RRSP room — is cleaner than carrying a loan and the audit risk indefinitely. I model both paths before you decide.

What documentation do I need for a CCPC shareholder loan?

Five items, all created before or on the day the money moves: a written loan agreement (two-page promissory note with principal, interest rate, repayment date); a director’s resolution in the minute book authorizing the loan; commercial-substance evidence of the loan’s purpose (purchase agreements, brokerage statements); contemporaneous bookkeeping showing the loan as a separate balance-sheet account with monthly reconciliation; and annual T-slip reporting for any imputed-interest benefit not eliminated by interest actually paid. The 2025 update to CRA’s interpretive guidance expressly tightened expectations on contemporaneous documentation — a loan agreement produced after an audit notice arrives is generally not credited.

Related Reading on This Site

- Do I Have to Pay 66.67% Capital Gains Tax If I Sell My Canadian Business in 2026? — Post 01 — the LCGE and surplus stripping rules interact with shareholder loan planning at exit

- Salary vs Dividends in 2026 — The Definitive Guide — Post 04 — the salary-vs-dividends decision is the companion question to “should I borrow from my corporation?”

- Do I Really Need a Holding Company? A 2026 Decision Framework — Post 03 — inter-corporate loans between HoldCo and OpCo carry their own shareholder-loan considerations

Conclusion and Next Steps

A shareholder loan from your CCPC is one of the highest-yield planning tools available to you — or one of the most expensive mistakes on your ledger. The difference is four decisions made in the first week, not four compliance steps done at year-end. Decide whether a loan is the right mechanism. Document it before the money moves. Calendar the repayment deadline with a 90-day warning. Design the repayment source as part of the original plan.

Owners who treat the shareholder loan account as a tactical, temporary tool with clean paperwork spend perhaps two hours a year on the documentation. Owners who don’t spend those two hours typically spend tens of thousands of dollars on an audit defence five years later. The 2025 CRA folios are a clear signal that the agency intends to enforce the regime with renewed vigour — planning that worked under the old guidance should not be assumed to survive the new framework without a fresh review.

Book a discovery call today to review your shareholder loan account and design compliant access to corporate capital → Book a complimentary 15-minute call

Important disclosure

General information only — not personalized investment, tax, or legal advice. Tax rules change frequently and your situation may differ materially from the examples above. The CRA prescribed interest rate is reset quarterly; the 3% rate cited throughout this post is the Q2 2026 rate effective April 1 through June 30, 2026 and may change in subsequent quarters. The shareholder-loan planning described here — loan design, documentation, repayment strategy — is properly executed with a financial planner designing the structure and a CPA handling the compliance execution. This post is a financial-planning overview, not a tax-preparation guide. Consult a qualified Canadian CFP and CPA before acting on anything in this post.

Author bio: Jahid Hassan is a CFA Charterholder and CFP Professional based in Calgary, Alberta, specializing in Investment Planning and tax integration for Canadian business owners. Connect on LinkedIn.

Pingback: Capital Gains Tax: Selling a Canadian Business in 2026

Pingback: Do I Need a Holding Company? 2026 Decision Guide

Pingback: Bonus, Salary or Dividend Before Year-End? (2026)