The Clock Is Already Running

No, the 66.67% capital gains inclusion rate is not the law. The proposed increase was formally cancelled on March 21, 2025. The rate is 50% — half of any capital gain is taxable. In Alberta, the combined top effective capital gains rate is 24.00%.

That question is settled. The question that isn’t settled — and the one that determines whether your family keeps $1.8 million or $3 million on the same $3 million sale — is what you do in the years before a buyer calls. The highest-leverage planning moves in a Canadian business exit happen 5 years out, not 5 months out. By the time a letter of intent lands on your desk, the structure is largely locked. The founders who walk away with Strategy 4 outcomes started the conversation when a sale was a possibility, not when it was imminent.

This post is organized as a countdown — from 5 years before a sale to the sale year itself — because that is how the planning actually works. Each time horizon has moves that belong there and moves that are too late.

Key Takeaways

- The 66.67% inclusion rate is dead. The capital gains inclusion rate is 50% in 2026. Alberta’s combined top effective rate is 24.00%. That question is settled — stop reading about it and start planning around the questions that aren’t.

- The $1,275,000 Lifetime Capital Gains Exemption is the single largest planning lever. One person shelters $1,275,000. A family of four, structured correctly, shelters $5,100,000. The difference is a planning decision made years before the sale.

- QSBC qualification is a multi-year project, not a year-end test. The 90% active-asset test and the 24-month holding period fail when left to the months before close.

- Share sale versus asset sale is a planning decision, not a negotiation detail. The after-tax difference on a $3M transaction is roughly $472,000 — decided in the letter of intent, before your CPA is involved.

- Your CPA files the return in the year of sale. Your planner designs the exit structure 2–5 years earlier — and that structure determines 80% of the after-tax outcome.

What I do, what your CPA does

This post is the planning conversation — organized as a countdown because the planning has a sequence and most of it happens before your CPA touches the file. My role is the structural design in the years before exit: family-trust positioning, LCGE multiplication strategy, QSBC purification timeline, HoldCo coordination, AMT modelling, and the share-sale-versus-asset-sale decision that shapes your negotiation posture. Your CPA owns the execution in the year of sale: the T1 filing, the Schedule 3 capital gains calculation, the LCGE claim on Line 25400, and the AMT parallel computation. I don’t file your return. I design the structure that makes your CPA’s numbers as small as possible.

On this page

- The Clock Is Already Running

- Key Takeaways

- The Capital Gains Punchline: Same Sale, Four Structures

- 5 Years Out — Settle the Trust, Freeze the Value

- 3 Years Out — Purify and Position

- 1 Year Out — Confirm and Coordinate

- Sale Year — Execute and File

- The Exit Timeline at a Glance

- The Three Planning Failures I See Most

- Sources

- Frequently Asked Questions

- Conclusion and Next Steps

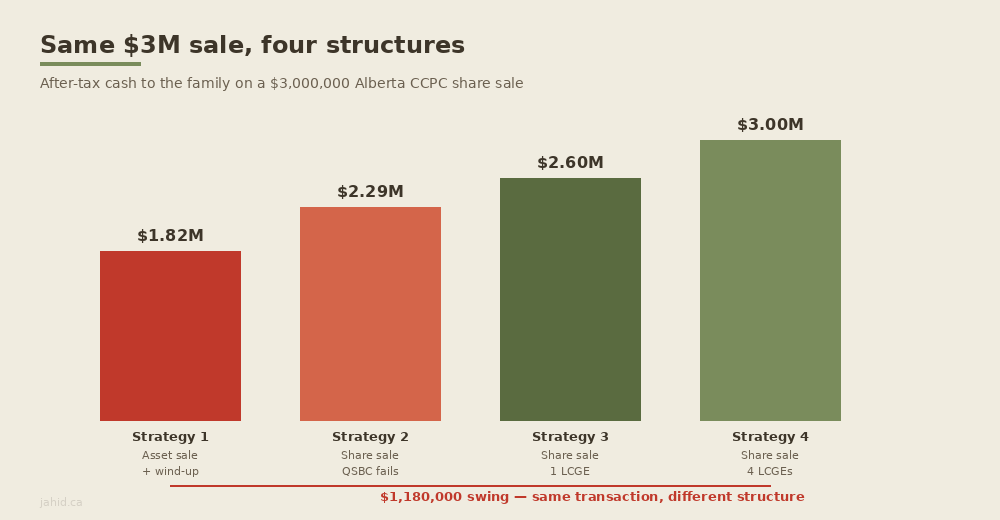

The Capital Gains Punchline: Same Sale, Four Structures

Before the countdown, the stakes. This case study is composite — the figures are realistic for an Alberta CCPC owner in 2026 but not a recommendation for any specific reader.

Scenario: Raj, a Calgary-based incorporated professional. Sole shareholder of an Alberta CCPC operating an active business for 15 years. A strategic buyer offers $3,000,000 for the shares. Adjusted cost base on the shares: $50,000. Capital gain: $2,950,000. Spouse and two adult children have been involved in the business at various stages.

| Strategy | What it means | Tax bill | After-tax to family |

|---|---|---|---|

| 1. Asset sale by corp, wind-up | Corp sells assets; proceeds extracted as ineligible dividend; no LCGE available | ~$1,180,000 | ~$1,820,000 |

| 2. Share sale, QSBC fails | Direct share sale; shares fail the 90% active-asset test — passive investments on the balance sheet | ~$708,000 | ~$2,292,000 |

| 3. Share sale, one LCGE claimed | Direct share sale; QSBC-qualified; Raj claims his full $1,275,000 LCGE | ~$402,000 | ~$2,598,000 |

| 4. Share sale, family LCGE multiplied | Family trust holds growth shares; LCGE claimed by Raj, spouse, and two adult children ($5,100,000 total exemption, exceeds the gain) | ~$0 | ~$3,000,000 |

The swing from Strategy 1 to Strategy 4 is $1,180,000 of family wealth — on the same $3,000,000 transaction with the same buyer. Strategy 4 requires a family trust or share-ownership structure put in place years before the sale. It cannot be retro-fitted in the months before close.

It is also worth noting what changes if the 66.67% inclusion rate had survived. On the same $2,950,000 gain in Strategy 3, the effective rate would have risen from 24.00% to roughly 32.00% on the portion above $250,000, adding approximately $236,000 of incremental personal tax. The cancellation is not abstract — it is six figures of after-tax cash for a single Alberta family.

What separates Strategy 1 families from Strategy 4 families is not cleverness at closing. It is the following countdown.

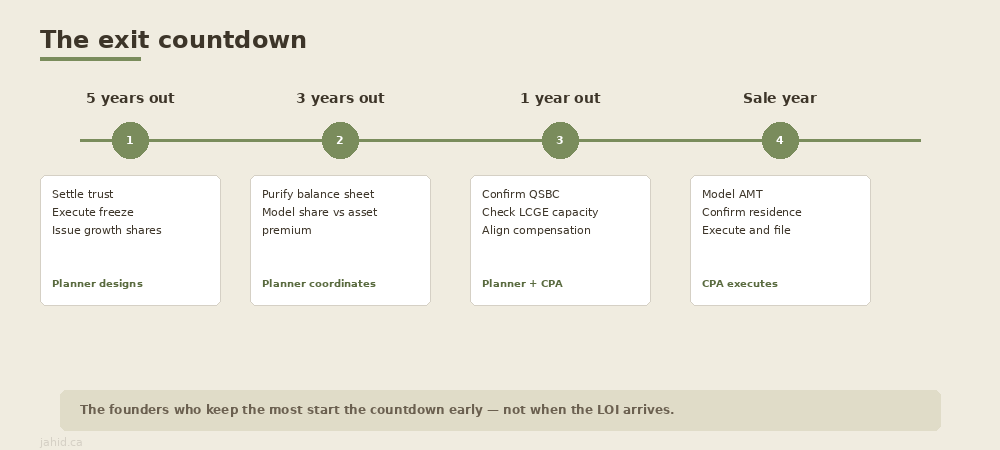

5 Years Out — Settle the Trust, Freeze the Value

Five years before a contemplated sale is when the highest-leverage moves are available, because the calendar is wide open and CRA cannot characterize the structure as a last-minute manoeuvre.

The family trust decision

The single biggest swing in the case study — from $402,000 of tax (Strategy 3) to roughly $0 (Strategy 4) — requires a discretionary family trust holding growth shares in the corporation. The trust enables LCGE multiplication: each adult beneficiary (spouse, children, grandchildren) has their own $1,275,000 personal LCGE in 2026, and on a sale the trust allocates capital gain across multiple beneficiaries — each claiming their own exemption.

Lifetime Capital Gains Exemption (LCGE)

A personal, once-in-a-lifetime deduction in section 110.6 of the Income Tax Act that shelters eligible capital gains from federal and provincial tax. For 2026, the LCGE limit on Qualified Small Business Corporation shares is $1,275,000 per individual taxpayer. A family of four can collectively shelter up to $5,100,000.

A family trust needs to have been settled and funded with growth shares for long enough that CRA cannot treat it as a last-minute tax manoeuvre. The qualification holding period runs from the trust’s acquisition of the shares, not from the founder’s original purchase. And the trust creates its own obligations: annual trust returns, TOSI compliance on every distribution, and a 21-year deemed-disposition clock that starts the day the trust is settled.

Five years is the comfortable window. Three years is tight. One year is too late for most trust structures to be defensible on audit.

The full planning framework is in the estate freeze + family trust playbook. My role is the decision — whether to freeze, when, with what trust structure, and how it integrates with your retirement timeline and investment plan. The tax lawyer drafts the trust deed and corporate amendments. The CPA files the annual returns and integrates the freeze into the corporate books.

The estate freeze

An estate freeze typically accompanies the family trust. The freeze exchanges your common shares for fixed-value preferred shares, capping your personal capital-gains exposure at today’s corporate value. New growth shares — issued to the family trust at nominal value — capture all future appreciation. On a sale five or ten years later, the growth accrued in the trust is allocated to beneficiaries who each claim their own LCGE.

The planning question at year five: is your corporation worth enough to freeze, and is it likely to appreciate materially before sale? A freeze on a corporation that is unlikely to grow further delivers little benefit. A freeze on a corporation worth $2 million and growing 15% per year delivers a lifetime of LCGE-sheltered appreciation for your family.

The Canadian Entrepreneurs’ Incentive — treat as not in force

The Canadian Entrepreneurs’ Incentive (CEI) was a 2024 budget measure proposing a reduced one-third inclusion rate on up to $2,000,000 of qualifying founder gains. Budget 2025 appears to have cancelled it, but the legislative text has not been formally repealed. For 2026 planning, we treat the CEI as not in force. If it is revived, anyone who has already structured a clean QSBC sale and family trust can layer it on top — nothing about planning without it creates downside.

3 Years Out — Purify and Position

Three years before a sale is the operational planning window. The structural decisions from year five are in place; now the corporation needs to satisfy the tests that make those structures work.

Will your shares qualify for the exemption? Three questions your planner checks

The LCGE only applies to shares that pass three qualification tests at the moment of sale. These are not obscure technicalities — they are planning checkpoints, and the most common reason a business owner loses the LCGE is not that the rules are hard, but that nobody checked until it was too late to fix.

Qualified Small Business Corporation (QSBC) share

A share of a privately-held Canadian corporation where, at the time of sale, at least 90% of the corporation’s value is tied to the active business, and for the full 24 months before the sale, more than half the assets were active-business assets and the shares were held by you or a related person.

Question 1 — Is your balance sheet clean enough? At the moment of sale, 90% or more of your corporation’s value must be in active-business assets. Surplus cash, a brokerage account, vacant land, life insurance cash value — all count against you. A corporation running a perfectly healthy operating business can fail this test if 12% of its balance sheet is sitting in investments. Raj’s OpCo had $340,000 in a diversified portfolio — 11.3% of the corporation’s $3,000,000 fair market value. One dividend to a holding company, 26 months before close, swept the passive assets off the balance sheet and restored the ratio with time to spare.

Question 2 — Has the balance sheet been clean long enough? For the full 24 months leading up to the sale, more than half the corporation’s assets must have been active-business assets. A less demanding threshold than Question 1, but it runs backward — a founder who reorganizes 18 months before close may not have enough runway.

Question 3 — Have you held the shares long enough? You (or a related person) must have owned the shares for the full 24 months preceding the sale. The trap: founders who sell OpCo shares to a newly-incorporated HoldCo, then sell the HoldCo shares a year later, restart the clock and lose the exemption. There are rollover mechanisms in the Income Tax Act that can preserve the holding period — but only when your tax lawyer invokes them deliberately during the reorganization, not after the fact.

The planning lever: These three questions are why purification is a 24+ month project. Three years out is the window to identify passive assets, sweep them to a holding company, and let the seasoning clock run. I design the purification timeline and coordinate with the CPA who runs the numbers and the lawyer who documents the transfer.

Share sale versus asset sale positioning

The other three-year planning move: deciding — before any buyer appears — whether you will insist on a share sale or accept an asset sale, and what premium would make you switch.

When a corporation sells its operating assets (equipment, goodwill, inventory, real estate), the corporation itself realizes the gain. The proceeds sit inside the corporation until you extract them as a taxable dividend — and the combined corporate-then-personal tax is substantially higher than what you would pay on a direct share sale, even before the LCGE.

On Raj’s $3,000,000 deal, the after-tax difference between asset sale (Strategy 1, ~$1,180,000 tax) and share sale before LCGE (Strategy 2, ~$708,000 tax) is $472,000. That gap is the buyer’s negotiation leverage — they want an asset sale because it lets them write off the purchase price faster and leave behind unknown liabilities. They will often pay a premium for it. Your job, with your planner, is to know the exact dollar figure where that premium compensates for the tax you give up. Without that number modelled in advance, you are negotiating blind on the variable that matters most.

1 Year Out — Confirm and Coordinate

By 12 months before a sale, the structure should be in place and the planning shifts from design to confirmation.

QSBC confirmation

Run the 90% active-asset test against the current balance sheet. If the purification from year three held — passive assets are in the HoldCo, operating assets are clean — the test should pass. If the OpCo has accumulated new surplus cash or investments in the intervening years, a second sweep may be needed. The 24-month holding-period test now runs backward from an expected sale date in the next 12 months — confirming the shares have been held by the vendor or a related person throughout.

LCGE capacity check

Confirm each family member’s available LCGE. The exemption is cumulative and lifetime — prior QSBC dispositions or farm-property claims reduce the remaining room. If a beneficiary used $400,000 of their LCGE on a prior transaction, their remaining room is $875,000 in 2026. This check shapes the trustee’s allocation strategy on the eventual sale.

Compensation strategy for the sale year

The salary-vs-dividends decision changes in the year before a sale. Drawing aggressive salary to keep cash out of the operating company preserves the 90% active-asset ratio. Owners sometimes try to bypass salary and dividend tax by routing cash through a shareholder loan instead, but the one-year repayment rule under subsection 15(2.6) and the section 80.4 imputed-interest benefit make this a high-risk substitute — especially in the year leading up to a sale, when CRA scrutiny intensifies. Leaving surplus earnings inside the corporation — whether as salary you did not draw or dividends you deferred — risks tipping the QSBC test at the worst possible moment. The one-year-out compensation plan should be coordinated between planner and CPA with the sale timeline in mind.

Assembling the team

By one year out, three professionals should be working in coordination: the financial planner (exit-structure design, AMT modelling, family-wealth integration), the tax lawyer (share-purchase agreement review, anti-avoidance analysis if the buyer is non-arm’s length, intergenerational-transfer conditions if selling to family), and the CPA (corporate-year-end positioning, qualification test documentation, sale-year return preparation). These three roles intersect at multiple points; the founders who get the best outcomes engage all three before the letter of intent is signed, not after.

Sale Year — Execute and File

The planning is done. The sale year is execution — your CPA’s territory — with two items where the planner and CPA work shoulder to shoulder.

The AMT surprise — when the exemption gives back less than you expected

Alternative Minimum Tax (AMT)

A parallel tax calculation that adds back a portion of the gain you sheltered with the LCGE and applies a flat rate above an annual exemption. If this parallel bill exceeds your regular tax, you pay the higher amount. The difference is recoverable as a credit over the following seven years — but only if you have enough regular tax in those years to absorb it.

The AMT is the rule that turns a “tax-free” LCGE claim into “mostly tax-free, with an asterisk.” On Raj’s numbers — a $2,950,000 gain with a $1,275,000 LCGE claim — the AMT adds back 30% of the sheltered gain ($382,500) into the parallel calculation. If Raj sells and retires with low future income, the seven-year credit may never fully offset — and the AMT becomes a permanent cost, not a timing difference.

The planning lever: Model AMT explicitly before the sale closes. Consider staging the sale across two tax years if the exposure justifies it. Consider deliberate income-creation strategies in the carry-forward window to absorb the credit. I run the scenario model; the CPA computes the parallel calculation on the actual return.

Provincial residence

The capital gains rate is set by your province of residence on December 31 of the sale year. Alberta’s 24.00% top effective rate compares to Ontario’s 26.77%, British Columbia’s 26.75%, and Quebec’s 26.65%. On a $2,950,000 gain, the Alberta-to-Ontario swing alone is roughly $82,000.

For an Alberta-based founder who lives and works here, this is simply the rate. For a vendor who has been on assignment out-of-province or who maintains residential ties elsewhere, the residency question can be litigated by CRA. A clear, documented provincial-residence trail in the calendar year of sale is part of the file your CPA assembles.

Selling to family — a different set of rules entirely

If the buyer is a corporation owned by your children or other family members — the classic intergenerational transfer — a separate anti-avoidance regime can recharacterize your capital gain as a fully-taxable dividend, wiping out the LCGE entirely. Federal legislation now allows a controlled exception for genuine family transfers, but the conditions are narrow: on the “immediate” track, you give up control within 36 months; on the “gradual” track, over 10 years. The rules were tightened materially in 2024, and the general anti-avoidance regime now includes an economic-substance test and a 25% misuse penalty. Any sale to a family member in 2026 should be reviewed against the current legislation by a tax lawyer — not the version that was in place when the deal was first discussed.

The Exit Timeline at a Glance

| Time horizon | Planning move | Who owns it | Cost of skipping |

|---|---|---|---|

| 5 years out | Settle family trust, execute estate freeze, issue growth shares to trust | Planner designs; tax lawyer drafts; CPA files | Loss of LCGE multiplication — up to $1,180,000 on a $3M sale |

| 3 years out | Purify OpCo (sweep passive assets to HoldCo), model share-sale vs asset-sale premium | Planner coordinates; CPA runs numbers; lawyer documents | QSBC failure — $306,000 lost per unused LCGE |

| 1 year out | Confirm QSBC, check LCGE capacity per beneficiary, align compensation strategy | Planner and CPA jointly | Surplus cash tips the 90% test at the worst moment |

| Sale year | Model AMT, confirm provincial residence, execute and file | CPA executes; planner models AMT staging | AMT becomes permanent cost; wrong province adds ~$82,000 |

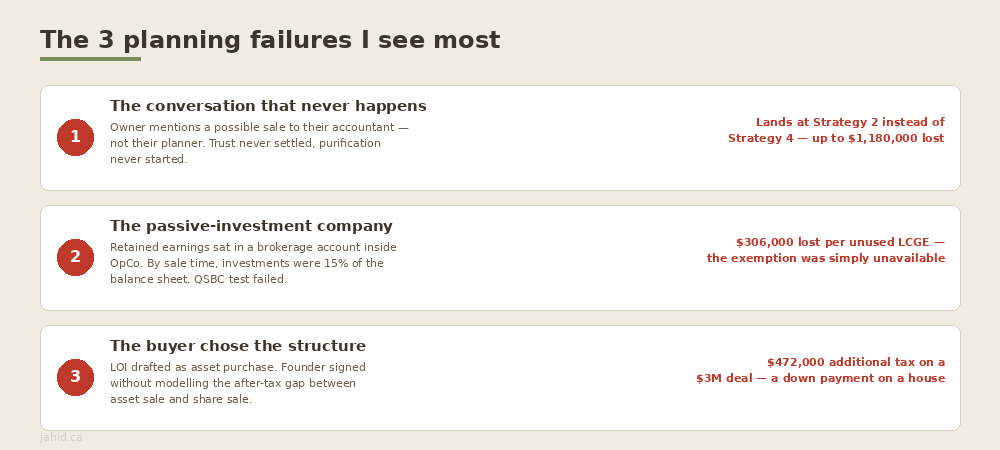

The Three Planning Failures I See Most

After working with CCPC owners in Calgary planning business exits, three patterns account for the majority of avoidable tax damage. Each one is a timing failure, not a knowledge failure — the founders knew the rules, they just started too late.

Failure 1: The conversation that never happens. The most common planning failure is not a mistake — it is a silence. A CCPC owner mentions to their accountant, casually, that they might sell in a few years. The accountant nods, files the year-end return, and the conversation does not happen again until a letter of intent arrives two years later. By then the family trust was never settled, the purification was never started, and the exit lands at Strategy 2 or 3 instead of Strategy 4. The fix is absurdly simple: mention to your financial planner, not just your accountant, that a sale is a possibility. That single conversation, three to five years before the event, is the one that opens the Strategy 4 door.

Failure 2: The operating company that quietly became a passive-investment company. The founder built a great business and retained earnings year after year — which is the right thing to do. But the retained earnings sat in a brokerage account inside the operating company, and by the time a buyer appeared, the investment portfolio was 15% of the balance sheet. The 90% active-asset test failed, and the $1,275,000 LCGE was unavailable. The purification that would have fixed it — a tax-free inter-corporate dividend to a holding company — needed 24 months of seasoning the founder did not have. A three-year-out HoldCo setup and systematic sweep would have prevented it entirely.

Failure 3: The share-sale-versus-asset-sale decision made by the buyer. The buyer’s lawyer drafts the letter of intent as an asset purchase — standard for buyers who want step-up and liability protection. The founder, unadvised on the after-tax difference, signs the LOI without modelling the gap. On Raj’s $3,000,000 deal, the gap between asset sale and share sale (before LCGE) is $472,000 of additional tax. That is not a rounding error — it is a down payment on a house. The fix: model the after-tax outcome of both structures with your planner before entering negotiations, and know the premium that makes you indifferent.

Sources

The statutory provisions referenced in this post (for readers and professionals who want the primary text):

- Income Tax Act — Section 110.6 (Lifetime Capital Gains Exemption)

- Income Tax Act — Section 84.1 (Non-arm’s length sale of shares — surplus stripping)

- Income Tax Act — Section 86 (Share-for-share exchange — estate freeze mechanism)

- Income Tax Act — Section 85 (Transfer of property to a corporation — rollover)

- Income Tax Act — Section 51 (Convertible property — alternative freeze mechanism)

- Income Tax Act — Section 112 (Intercorporate dividend deduction — tax-free sweep to HoldCo)

- Department of Finance Canada — Cancellation of capital gains inclusion rate increase (March 21, 2025)

- Canada Revenue Agency — Line 25400 Capital gains deduction

- Canadian Federation of Independent Business — Capital Gains Changes brief

- FP Canada — Standards of Professional Responsibility

Frequently Asked Questions

What is the Lifetime Capital Gains Exemption (LCGE) limit for a CCPC in 2026?

The LCGE limit for Qualified Small Business Corporation shares is $1,275,000 per individual in 2026, indexed annually thereafter. Each individual has a single lifetime exemption — a family of four with appropriately structured share ownership can collectively shelter up to $5,100,000 of capital gains on a single business sale. The exemption applies only to dispositions of QSBC shares (and certain farm and fishing property); it does not apply to public-company shares, real estate, or assets sold by a corporation. The planning question is not whether the exemption exists — it is whether your share structure and family trust position multiple family members to claim it, which is a design decision made years before the sale.

What are the rules for intergenerational family business transfers (Bill C-208) in 2026?

Bill C-208, refined by the 2024 federal amendments, allows a parent to sell shares of a qualifying family business to a corporation owned by adult children without triggering section 84.1 surplus stripping rules, provided either the “immediate” transfer conditions (control given up within 36 months) or the “gradual” transfer conditions (control given up over 10 years) are met. Both tracks require the children to actively engage in the business for prescribed periods. In 2026 the rules are materially tighter than the original 2021 legislation — any intergenerational transfer should be reviewed against the current version before signing a share purchase agreement. The planning work is designing a succession structure that satisfies the conditions; the CPA and tax lawyer execute the documentation and filing.

How do I set up an estate freeze for my incorporated business in Alberta?

An estate freeze locks in the current fair market value of your corporation as your personal tax liability and shifts all future growth to the next generation — typically through a family trust holding new growth shares. The mechanics use section 86 or section 51 of the Income Tax Act. The full planning framework is in the estate freeze playbook. My role is the planning decision — whether and when to freeze, how it integrates with your exit timeline and LCGE multiplication strategy. The tax lawyer drafts the documents; the CPA files the elections. The freeze belongs in the “5 years out” window of this countdown — not the year before sale.

How does surplus stripping work after the recent Department of Finance updates?

Surplus stripping — converting taxable dividends into lower-taxed capital gains by selling shares to a non-arm’s-length purchaser — is functionally unavailable outside the genuine intergenerational transfer corridor in 2026. Section 84.1 was tightened in 2024. The general anti-avoidance rule (GAAR), effective January 1, 2024 with an economic-substance test and a 25% misuse penalty, backstops the specific provisions. Structures that worked under earlier law should be reviewed against the current regime. Design new structures assuming the post-2024 regime is the floor of future enforcement, and structure exits with your planner, CPA, and tax lawyer working as a coordinated team.

Related Reading on This Site

- Do I Really Need a Holding Company? A 2026 Decision Framework — Post 03 — the HoldCo is the vehicle for QSBC purification at year 3 of the countdown

- Salary vs Dividends in 2026 — The Definitive Guide — Post 04 — your compensation strategy in the years before sale affects how much passive investment sits inside the OpCo

- The Estate Freeze + Family Trust Playbook for 2026 — Post 05 — the year-5 move; the trust structure that enables LCGE multiplication across your family

- TOSI in 2026: How Income-Splitting Constraints Shape Your Family-Compensation Strategy — Post 06 — TOSI governs every trust distribution between the freeze and the sale, and can surface in the sale year itself

Conclusion and Next Steps

The exit clock is already running. The founders who keep the most are not the ones with the cleverest tax position at close — they are the ones who started the countdown early enough that every move had time to season.

Five years out: settle the trust and freeze the value. Three years out: purify the balance sheet and model the share-sale premium. One year out: confirm the QSBC tests and coordinate the team. Sale year: execute and file.

If a sale is even a possibility in the next 3–7 years, the right next step is a planning conversation — not about what the buyer will offer, but about what structure will be in place when they do.

Book a discovery call today to find out where you are on this countdown → Book a complimentary 15-minute call

Important disclosure

General information only — not personalized investment, tax, or legal advice. Tax rules change frequently and your situation may differ materially from the case study above. The Canadian Entrepreneurs’ Incentive (CEI) is treated in this post as not in force based on Budget 2025 signals; legislative text has not been formally repealed and may be revisited in a future budget. The exit-planning structure described here — LCGE multiplication, QSBC purification, family-trust design — is properly executed by a coordinated team of financial planner, tax lawyer, and CPA. This post is a financial-planning overview, not a legal opinion or a tax-preparation guide. Consult a qualified Canadian CFP, CPA, and tax lawyer before acting on anything in this post.

Author bio: Jahid Hassan is a CFA Charterholder and CFP Professional based in Calgary, Alberta, specializing in Investment Planning and tax integration for Canadian business owners. Connect on LinkedIn.

Pingback: Do I Need a Holding Company? 2026 Decision Guide